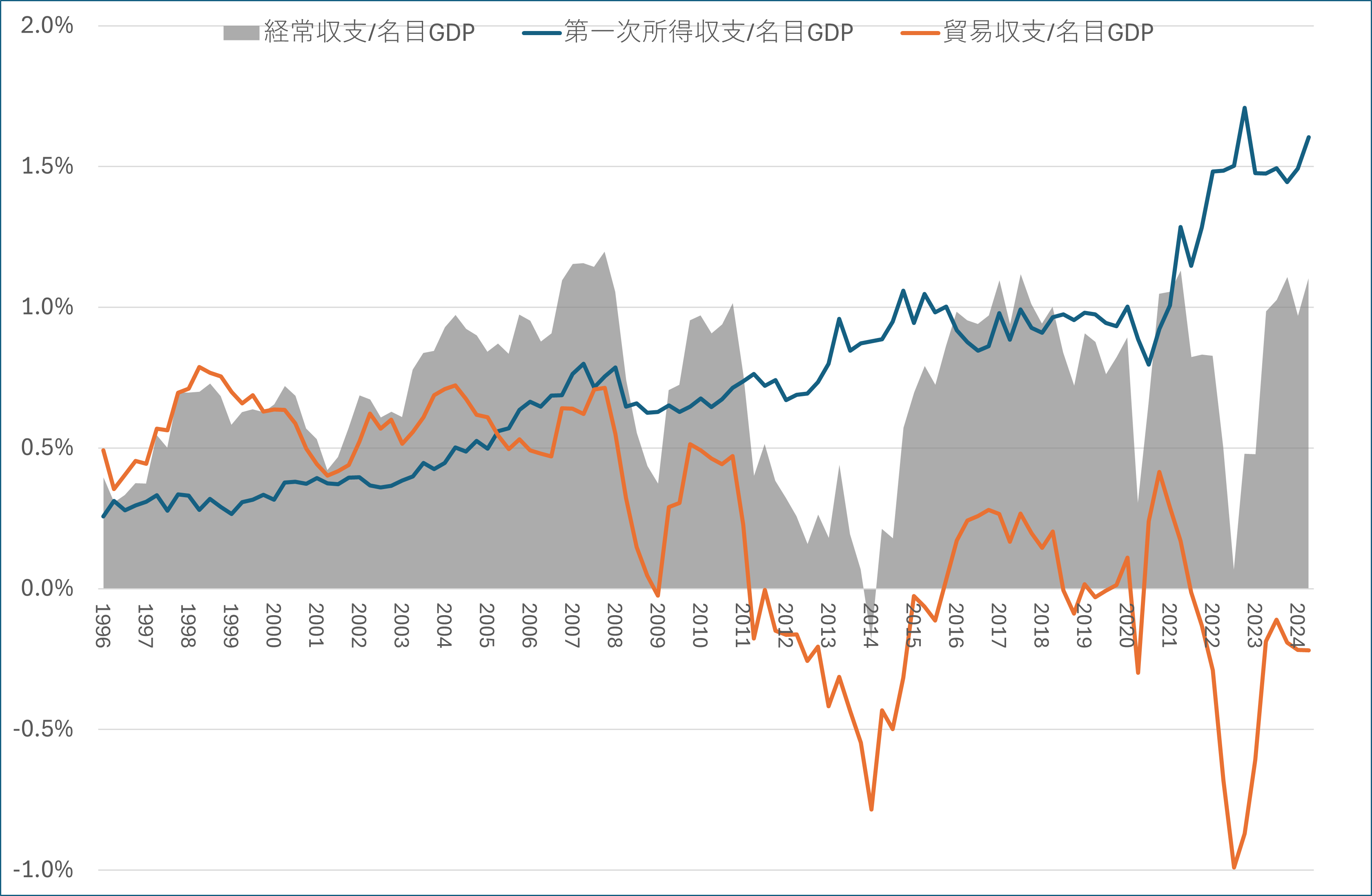

Do All Roads Lead to Terms of Trade? (1)

On August 15, the Cabinet Office released the preliminary GDP report for the second quarter of 2024. Upon updating the Buffett Indicator as seen in the August 1 post, the stock market remains in overvalued territory, but the forecasted PER is within the appropriate range. As mentioned in the August 4 post, this is due to the increase in corporate income from overseas.

Stock Market Remains Overvalued According to the Buffett Indicator, but Forecasted PER is Within the Appropriate Range

The GDP announced this time is up to the second quarter (April to June), so using the TOPIX at the end of June, I calculated the Buffett Indicator average and standard deviation from the first quarter of 1994 to the second quarter of 2024, as well as the zone of average ± 1 standard deviation.

Additionally, I included the value using the GDP (nominal, seasonally adjusted) for the second quarter of the same year and the closing price of TOPIX on August 16 (2,678.60) (the red line in the graph). While the stock market remains in overvalued territory, the forecasted PER (as reported in the Nikkei Newspaper: Domestic Stock Indexes, TSE (16th)) at the close on the 16th is 15.47 times, which is within the appropriate range.

As mentioned in the August 4 post, the reason why the forecasted PER is appropriate even though the Buffett Indicator shows an overvaluation is due to its similarity with other economic indicators. One such indicator is the primary income balance in the balance of payments created by the Ministry of Finance.

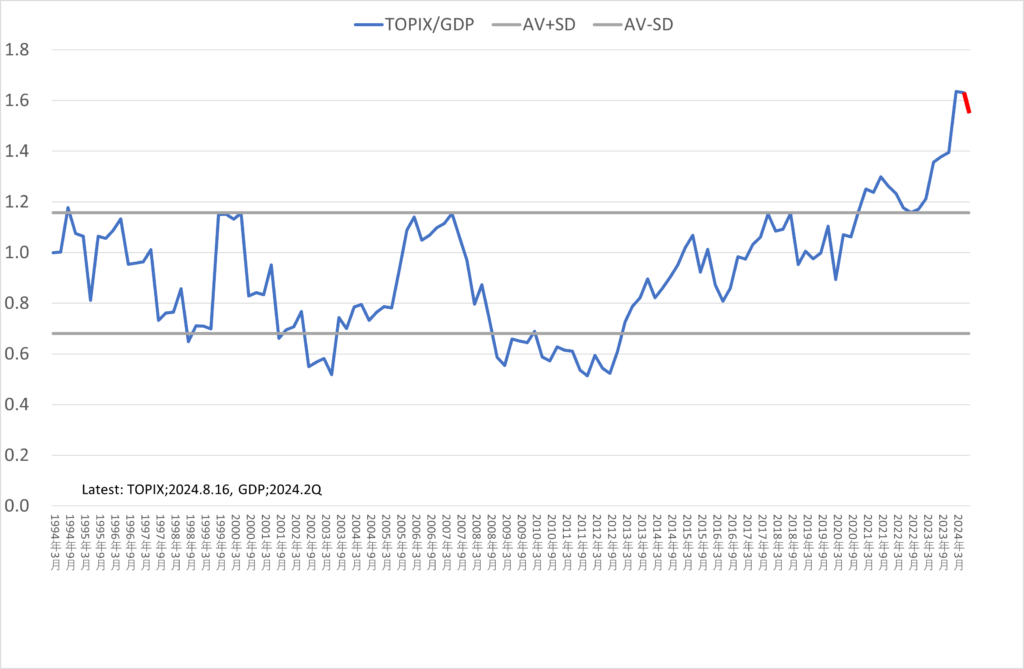

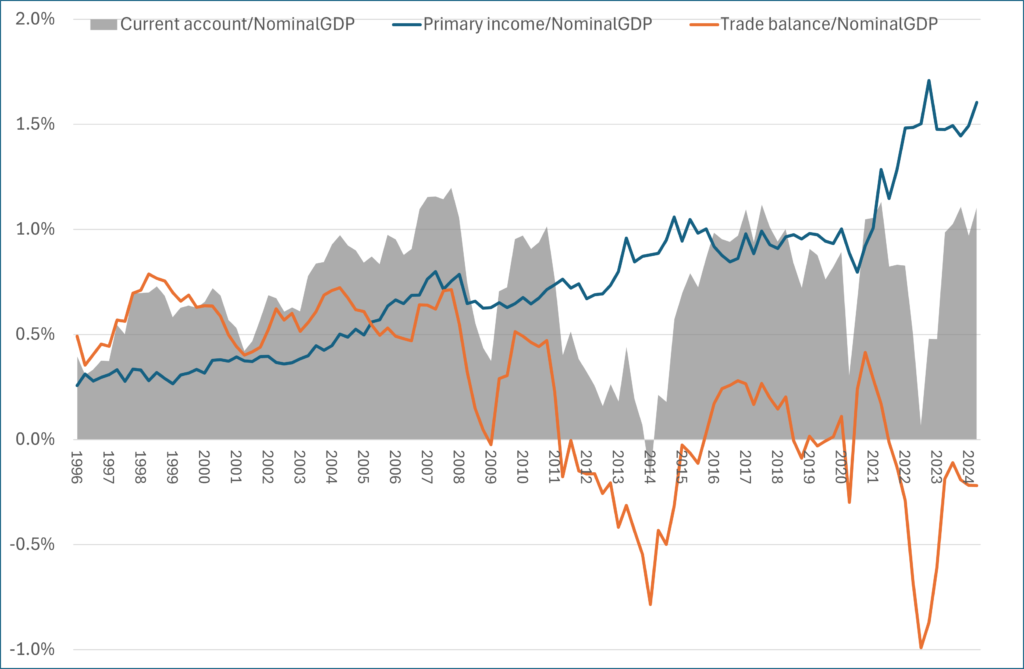

Even with a Trade Deficit, the Primary Income Balance is in Surplus

Interest and dividend income from overseas are not directly confirmed in the GDP tables created by the Cabinet Office, but they are confirmed in the “Primary Income Balance (Interest and Dividend Income from Overseas)” in the balance of payments. Here, I am using seasonally adjusted figures available since 1996 and looking at them as a percentage of nominal GDP (seasonally adjusted).

It is confirmed that the ratio of the primary income balance has sharply increased since 2020, accompanying the depreciation of the yen.

Japan used to have a constant trade surplus, but since 2009, trade deficits have become more common. However, due to the increasing surplus in the primary income balance, the current account (the total of the primary income balance, secondary income balance, and trade and services balance) has continued to be in surplus, except for 2014.

Focusing on the period since 2021, despite the yen’s depreciation, the trade deficit remains. The background to this involves issues related to the currency denomination of traded goods and fluctuations in trade volumes, which require separate consideration. However, in line with the discussion in previous posts, I want to highlight the sharp increase in the ratio of the primary income balance to GDP since 2021.

One reason is that the yen’s depreciation has led to an increase in the yen-equivalent amount, but it also seems to be related to the terms of trade and trading gains/losses.

The term “terms of trade” has been appearing frequently lately. There’s a saying, “All roads lead to Rome,” but it seems that various factors are leading to terms of trade. In future posts, I plan to examine terms of trade and trade gains/losses.

\ 最新情報をチェック /