日本語は次ページ

In my previous post, I discussed the narrowing interest rate gap between Japan and the US. The interest rates covered were nominal interest rates. This time, I will also mention the “Real Interest Rate Parity” (RIRP), which explains exchange rate movements using real interest rates.

Nominal Interest Rates

The interest rates we usually use are called nominal interest rates, which do not take price changes into account.

Inflation

Inflation is a phenomenon where prices rise overall. When the inflation rate (the rate of increase in prices) is high, the value of money decreases, reducing the amount you can buy with the same amount of money.

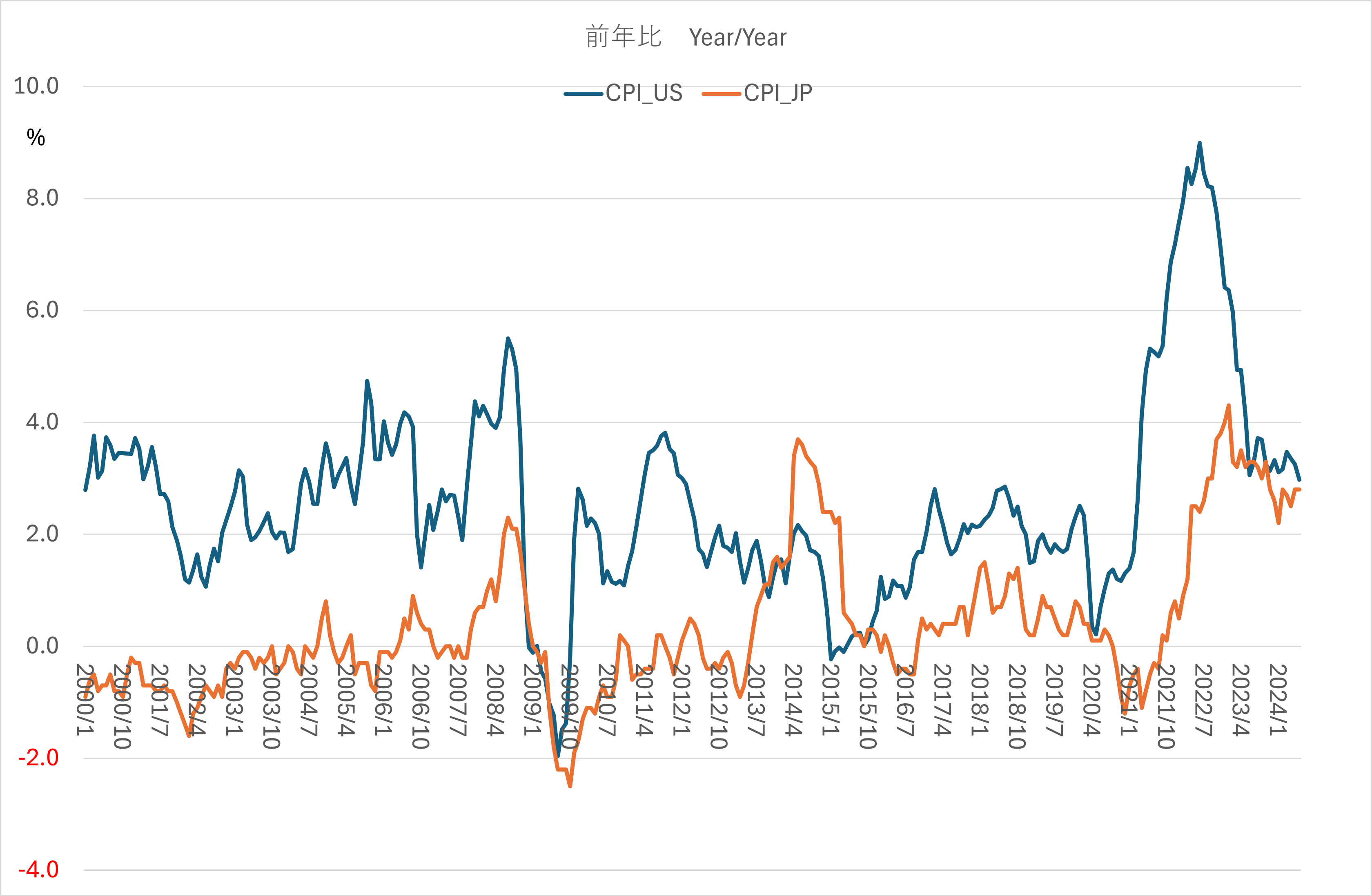

(Note) End-of-month values up to June 2024

(Source) US CPI: St. Louis Fed FRED, Japan CPI: Ministry of Internal Affairs and Communications e-Stat

Looking at the year-on-year Consumer Price Index (CPI), the inflation rate in the US has been rapidly declining and was even below that of Japan in June 2023. Recently, it has only slightly surpassed Japan’s.

Real Interest Rates

Real interest rates, which consider the “actual value changes,” are the nominal interest rates minus the expected inflation rate. For example, if the nominal interest rate is 5% and the expected inflation rate is 2%, the real interest rate is 3%.

Currency Appreciation in Countries with High Real Interest Rates

In countries with high real interest rates, the real return on investment is expected to be high.

For example, if you invest in assets of a country with a nominal interest rate of 5%, the total amount of principal and interest after one year will be 1.05 times the investment amount. However, if the price level in that country is expected to rise by 10% during that period, the real value of the assets in terms of goods in that country decreases by 5% (5% – 10% = -5%).

Therefore, when investors decide where to invest their money, they move their funds to countries with high real interest rates, which is the basic concept of the Real Interest Rate Parity. In this case, funds move from countries with low real interest rates to those with high real interest rates, increasing the value of the latter’s currency.

Using Expected Inflation Rates for Real Interest Rates

Since interest rates are the price of borrowing and lending money from the present to the future, we must use the expected inflation rate from the present to the future, not the historical inflation rate.

However, since the expected inflation rate is literally a forecast value, it cannot be observed numerically. Therefore, as a second-best measure, the historical inflation rate is used as a proxy for the expected inflation rate.

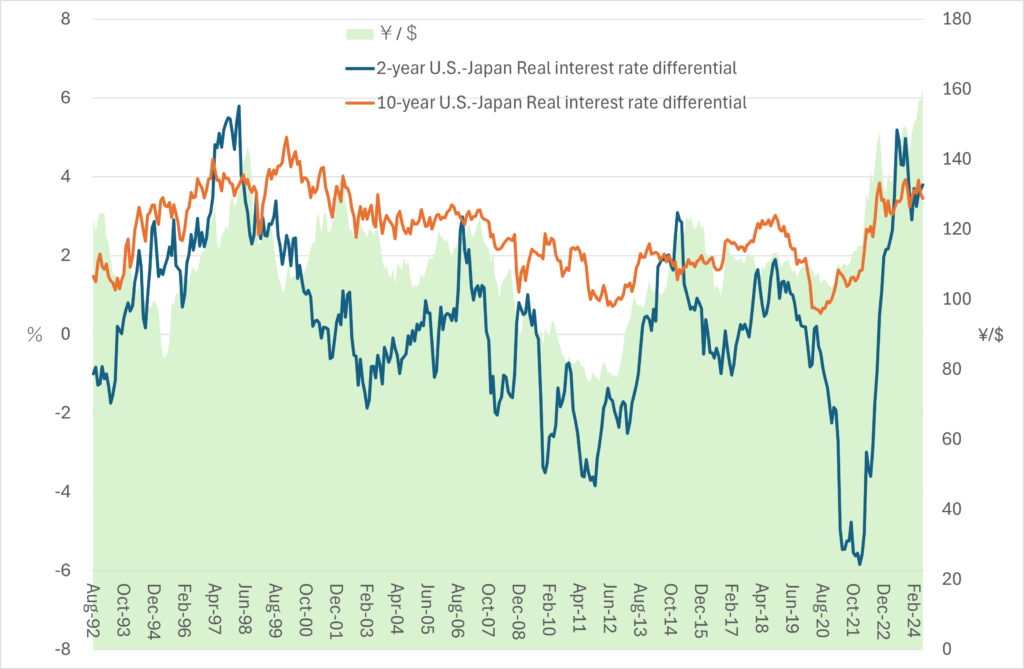

As of the end of June 2024, the US 10-year interest rate is 4.5%, and the year-on-year CPI (actual) is 3.0%, making the real interest rate 1.5% positive. On the other hand, Japan’s 10-year interest rate is 1.1%, and the year-on-year CPI (actual) is 2.8%, making the real interest rate 1.7% negative.

When we look at the real interest rate difference between the two countries, using the historical inflation rate as a proxy, it is almost the same as the nominal interest rate difference. However, the exchange rate trend seems to be more closely linked to the difference in the two-year real interest rates between Japan and the US than to the nominal interest rate difference.

This implies that if the expected inflation rate in the US declines faster than in Japan, the real interest rate gap will widen further, potentially leading to a stronger dollar and a weaker yen.

However, it is essential to note that the inflation rate determining the real interest rate is an expected value, not an actual value. The historical inflation rates used here do not necessarily move in the same direction as the expected inflation rates.

Another Point to Note

While it is beyond the scope of this discussion, it is necessary to distinguish whether the two variables are genuinely linked or just appear to be linked by coincidence.

There are cases where two randomly moving variables happen to show similar movements, which is called “spurious correlation.”

Therefore, it is necessary to conduct statistical hypothesis testing to determine if the interest rate difference and exchange rate trends are truly linked. However, considering the theory that they are linked, as introduced here, we assume it is not a “spurious correlation.”

Nevertheless, it is beneficial to have an intuitive understanding of what a “spurious correlation” is. Next time, we will simulate the behavior of two variables moving randomly and independently.

\ 最新情報をチェック /